The moments after a car accident are confusing and stressful. Between checking for injuries, swapping information, and dealing with police, insurance paperwork is the last thing on your mind. But once things calm down, you may face growing medical bills, time off work, and the hard task of finding out who pays.

This is where Personal Injury Protection (PIP) insurance becomes critical. Often called “no-fault” insurance, PIP covers your medical bills and lost wages, no matter who caused the accident. Understanding how this coverage works, and whether you have it, can mean the difference between stability and debt.

What Is Personal Injury Protection (PIP) Insurance?

Personal Injury Protection (PIP) insurance is part of your auto policy. It covers medical bills and other losses after a car accident. Unlike liability insurance, which pays for damage you cause to others, PIP pays for your expenses. It often covers your passengers’ expenses too, no matter who was at fault.

PIP is designed to provide quick financial support when you need it most. Instead of waiting for a long investigation to decide fault, you can file a claim with your insurer. You can then get paid quickly for covered costs.

What PIP Typically Covers:

- Medical and rehabilitation expenses – Hospital stays, surgeries, doctor visits, physical therapy, and even chiropractic care

- Lost wages – Compensation for income lost while you recover from your injuries

- Funeral expenses – In the tragic event of a fatal accident

- Replacement services – Costs for childcare, housekeeping, or other essential tasks you cannot perform while injured

The specifics of PIP coverage vary by state and insurer. In Texas, PIP is optional but highly recommended. Understanding your policy’s limits and exclusions is essential to avoiding surprises after an accident.

How Does PIP Insurance Work?

PIP insurance functions by providing compensation for expenses after an accident without requiring a determination of fault. This “no-fault” feature streamlines the claims process, allowing policyholders to access funds quickly.

When you file a PIP claim, you must provide documentation to support your expenses. This typically includes:

- Medical bills and treatment records

- Proof of lost wages (pay stubs, employer statements)

- Receipts for replacement services

- A completed claim form from your insurer

Once submitted, your insurance company reviews the documentation and, if approved, issues payment up to your policy’s coverage limits. The process is usually faster than filing a claim against another driver’s liability insurance. This is because there is no dispute about who caused the accident.

Important: Texas is an “at-fault” auto insurance state. The driver who caused the accident must pay for damages. However, PIP coverage operates independently of fault. Even if you caused the crash, your PIP benefits are still available to cover your medical bills and lost wages.

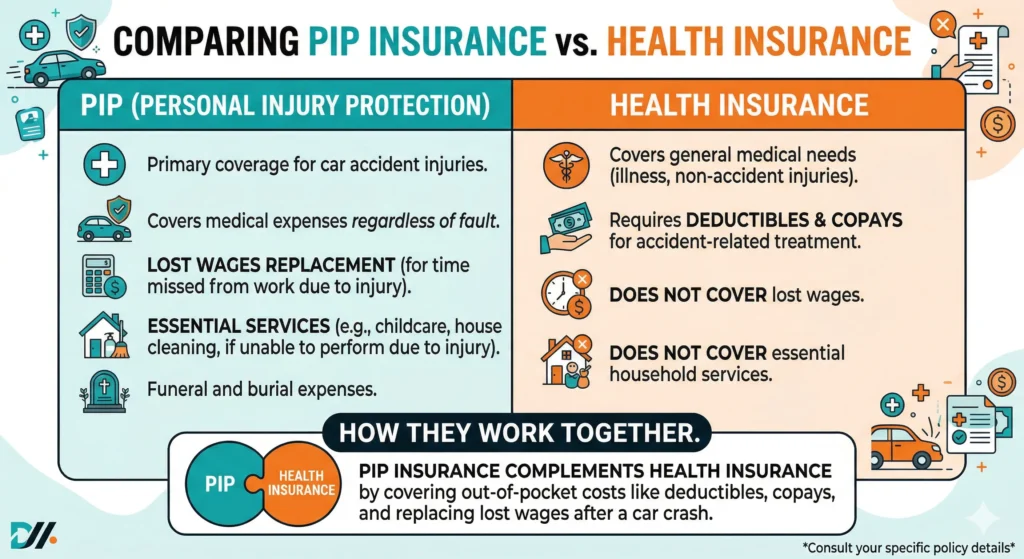

PIP Insurance vs. Health Insurance: What’s the Difference?

Many people assume their health insurance will cover car accident injuries. While health insurance does provide coverage, PIP offers distinct advantages:

| Feature | PIP Insurance | Health Insurance |

|---|---|---|

| Fault Consideration | Pays regardless of fault | Pays regardless of fault, but may require coordination |

| Speed of Payment | Fast; no fault investigation needed | May involve deductibles, copays, and pre-authorizations |

| Coverage Scope | Medical bills, lost wages, replacement services | Primarily medical expenses; often excludes lost wages |

| Subrogation | Generally not required to repay | May require repayment if you settle with another party |

PIP can supplement your health insurance. It can cover deductibles, copayments, and costs not covered by health insurance. This may include lost wages. Having both ensures you’re fully protected.

State Requirements and Coverage Limits in Texas

Unlike some states that mandate PIP coverage, Texas law makes it optional. However, insurance companies are required to offer PIP coverage to policyholders. You must actively reject it in writing if you choose not to carry it.

Texas PIP policies usually have a minimum coverage limit of $2,500. Higher limits, like $5,000, $10,000, or more, are also available. The coverage limit is the maximum amount your insurer will pay per person per accident.

Texas PIP Coverage Options:

- $2,500 minimum – Basic coverage for minor accidents

- $5,000 – More robust coverage for moderate injuries

- $10,000+ – Comprehensive coverage for serious accidents

Given the rising cost of medical care, the $2,500 minimum limit may run out fast. This is more likely if you need surgery or extended treatment. Opting for higher limits provides greater financial protection.

The Role of a Personal Injury Lawyer in PIP Claims

While PIP claims are generally simpler than liability claims, complications can arise. Insurance companies may delay payment, dispute the necessity of treatment, or attempt to deny coverage based on technicalities. When this happens, having an experienced personal injury attorney on your side is invaluable.

A lawyer can:

- Explain your policy’s terms and conditions so you understand what’s covered

- Handle all communication with the insurance company to prevent you from saying something that could harm your claim

- Ensure proper documentation is submitted to avoid delays

- File appeals or lawsuits if your claim is wrongfully denied

- Coordinate PIP benefits with other insurance to maximize your total recovery

If your PIP coverage does not pay all your costs, a personal injury lawyer can help. They can file a claim with the at-fault driver’s insurance for more money.

Maximizing Your PIP Benefits: Practical Tips

To make the most of your PIP coverage, proactive management is essential:

- Review Your Policy Today – Don’t wait until after an accident. Understand your coverage limits and whether you have PIP at all. If you only have the minimum $2,500, consider increasing it.

- Seek Medical Attention Immediately – Even if you feel fine, get checked out. Some injuries take days or weeks to appear. Delaying treatment can jeopardize your health and your claim.

- Document Everything – Keep a file of all medical bills, treatment records, prescriptions, and correspondence with your insurance company. Track any missed work and lost wages.

- Submit Claims Promptly – Don’t delay filing your PIP claim. The sooner you submit documentation, the sooner you’ll receive payment.

- Communicate Clearly with Your Insurer – Provide complete and accurate information. Incomplete paperwork is a common reason for claim delays.

- Consult an Attorney if Issues Arise – If your claim is denied, delayed, or the payout seems too low, don’t accept it. Contact a lawyer to review your options.

When to Contact an Injury Attorney

Knowing when to seek legal help can be critical to protecting your rights. Consider contacting an attorney if:

- Your PIP claim is denied for reasons that seem unjustified

- The insurance company is delaying payment without explanation

- Your medical bills exceed your PIP coverage limits and you need to pursue additional compensation

- The insurance company disputes the necessity of your medical treatment

- You’re unsure of your rights or overwhelmed by the claims process

A personal injury lawyer can handle these challenges. They help you get the full benefits you deserve under your policy and other sources.

Protecting Yourself with PIP Insurance

Car accidents are unpredictable, but your financial security doesn’t have to be. Personal Injury Protection insurance offers a safety net. It can cover medical bills and replace lost income. It also helps you focus on what matters most: your recovery.

In Texas, where PIP is optional, too many drivers forgo this coverage to save a few dollars on their premium. When an accident happens, they quickly realize the mistake. Don’t let that be you. Review your policy today, understand your coverage, and consider whether higher limits make sense for your situation.

And if you were in an accident and now face insurance claims, medical bills, or lost wages, you are not alone. The right advocate can make all the difference.

At Starr Law, P.C., we help injured Texans handle PIP claims and seek the compensation they deserve. Contact us today for a free, confidential consultation. Call 214-982-1408.

References

- Texas Transportation Code, Chapter 601 (Motor Vehicle Safety Responsibility Act)

- Texas Insurance Code, Article 5.06-1 (Personal Injury Protection Coverage)